Acorns Review 2025: Pros, Cons, Fees & How It Works

The Acorns app helps you save and invest your spare change. When you link a credit or debit card, Acorns rounds your purchase up to the nearest dollar and invests the difference. However, the monthly account fees will have an impact on your returns.

Some of the links on DollarSprout point to products or services from partners we trust. If you choose to make a purchase through one, we may earn a commission, which supports the ongoing maintenance and improvement of our site at no additional cost to you. Learn more.

Acorns Overview

How It Works: Acorns makes it easy for beginner investors to get started with investing in stocks. Set up one-time, recurring, or Round-Up deposits and watch your brokerage account balance grow.

Cost: $3, $5, or $9 per month plans.

- Pro: Round-Ups feature automates investing (incremental gains can reinforce the desire to save).

- Con: Higher fees than competitors.

Promotion: Exclusive $20 investment bonus for readers who set up recurring investments.

Best for: People who need to be forced into saving money.

I’ve always been skeptical of micro-investing apps. Can they really make a difference in my financial journey? With 15 years of investing experience under my belt, I’ve come to realize that I get the best results when I do the least amount of work. The less that I touch my investments, move money around, or even look at how I’m doing, the better things go. The minute I start micromanaging is usually the exact moment that I end up making a mistake.

So when it comes to investing apps, I prefer apps with fewer bells and whistles. I don’t need – or even want – all the fancy charts and second-by-second data. I just need something that will help me stay consistent and let me accumulate assets in low-cost index funds.

Acorns is an investing app that caters to people like me who want an easy-to-use interface and a hands-off investing experience. I recently decided to give Acorns a test drive and see for myself how it could fit into my financial life.

What Is Acorns?

Acorns is a financial technology and investment app — launched in August 2014 — geared towards making investing more accessible to the general public.

It automatically rounds up users’ everyday purchase amounts to the nearest dollar and invests the spare change into diversified, computer-managed portfolios. Acorns has amassed over 10 million users and claims $15 billion in assets under management.

Users generally appreciate the app for its user-friendly design and the ease with which it allows them to start investing, but some have raised concerns over the fees charged and the overall value for more experienced investors.

The Acorns app is best for new investors still learning the ropes. Notably, Acorns rounds up card-linked purchases to the nearest dollar and invests the extra change. Users can also set automatic recurring investments on a daily, weekly, or monthly basis. Current Promotion: Exclusive $20 bonus for new users.

Show Hide moreThe mobile application itself holds a 4.6-star (out of 5) rating on Google Play (284,000 reviews) and a 4.7-star rating on the App Store (875,000 reviews). It is #73 on the list of most downloaded Finance apps on the App Store with over 20 million downloads.

🔍 Reviewer’s Note:

Acorns' focus on automating investing will help users build up their savings; however, the high fees might do more harm than they're worth.

Acorns Subscription Plans & Features

As with many products in today’s subscription-focused environment, Acorns offers several different pricing tiers, each with its own set of additive features.

1. Acorns Personal

- Cost: $3 per month

I signed up for the cheapest plan with Acorns, which they call “Acorns Personal”. For $3 a month, here is what users get with an Acorns Personal account:

| What’s Included (in Acorns’ own words) | My Impression |

| Investing | |

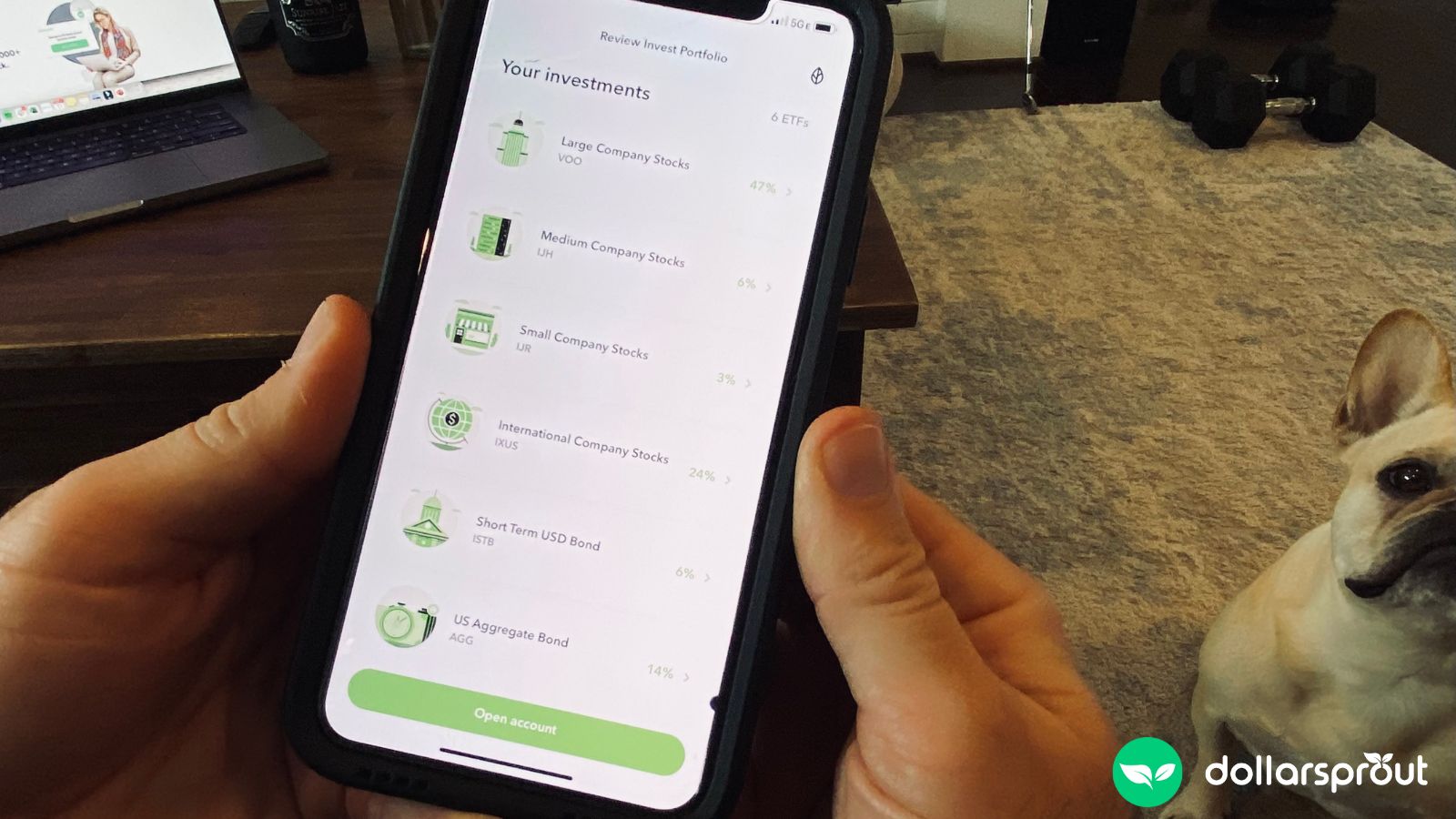

| Investment account with an expert-built, diversified portfolio | My recommended portfolio was 6 ETFs with very low expense ratios (none above 0.06%). Very good. |

| Save and invest spare change every day with Round-Ups® | Napkin math: If I use my card 3 times a day with an average of $0.50 rounded up, that would be equal to $45 a month invested. Thinking of it this way makes it easier for me to conceptualize as part of my budget, rather than the spare-change mindset. |

| IRA retirement account | A normal account type to offer, but I’m glad they have it. |

| Banking | |

| Checking account that saves and invests for you. | A neat feature, but not sure how impactful it really is. |

| Instantly invest spare change with Real-Time Round-Ups® | Before, you would need to accumulate $5 in Round-Ups before they were invested. Now it can be done instantly if you have an Acorns debit card. |

| No overdraft fees. Ever. | Nice. Hopefully, this trend continues to spread across the industry. |

| 55,000+ fee-free ATMs nationwide and around the world | Important to note that Acorns is not an actual bank. All Acorns checking accounts are issued by either Lincoln Savings Bank or nbkc Bank, members FDIC. |

| Earning | |

| 450+ in-app partner brands to earn bonus investments with. |

These partner brands pay Acorns to promote them to Acorns users and offer a commission to Acorns for each new customer. Acorns then passes some of that commission along to you, the user, in the form of a “bonus investment”. |

| Find a side hustle with Job Finder | Another cool feature, but nothing you can’t find through other websites or apps. |

| A browser extension to get bonus investments every time you shop at 15,000+ partners. | Basically, a cash back app that is integrated into Acorns. Cash back apps are free, but the functionality to direct the money into investments is nice. |

| Learning | |

| Grow your financial confidence with videos and tips for investors, both experienced and new. | Definitely geared more towards newer investors who are still learning the basics. Acorns does have a nice UX for providing easy-to-understand definitions for unfamiliar words that appear throughout the app. |

On the surface, it seems like you get a lot for $3 a month with Acorns, but I’ve found that almost everything on this list can be found for free elsewhere. But I don’t think the real value that Acorns delivers comes from its features, per se, but more from the overall behavior changes and habits that it can help you form.

For instance, a similar Round-Up feature is available via the Robinhood app for free, but many users find that Robinhood is a much more addictive app because of certain gamification tricks they use to get you to keep coming back. So while you might save $3 a month by using Robinhood instead of Acorns, you might end up wandering down a rabbit hole that you didn’t intend to go down — which can become much more costly.

🔍 Reviewer’s Note:

I ended up using my debit card 132 last month for purchases of all kinds: gas, groceries, assorted bills, Amazon, you name it -- ultimately, just over 4 times per day. Between $5 weekly recurring deposits and the added Round-Ups, I'm looking at just under $100 per month in cumulative deposits.

2. Acorns Personal Plus

- Cost: $5 per month

The next membership tier is Acorns Personal Plus, for $2 more per month. This plan comes with all the same features as the $3 Acorns Personal plan, with the addition of:

| Acorns Personal Plus Features (in Acorns’ own words) | My Impression |

| Emergency fund for life’s unexpected hiccups. | This is basically an extra account that is separate from your normal spending and investing accounts. This is usually free at most banks. |

| Get your bonus investments matched by Acorns (up to 25%) | The bonus investments are made by completing offers from brand partners of Acorns, so this is just an additional incentive for users to complete those offers (which you might not necessarily need). |

| Live Q+A with investment experts | This type of education is offered for free in many places. |

I personally don’t think these features are worth an additional $24 per year in subscription fees, but some users may appreciate these options more than I do.

- Cost: $9 per month (the Family Plan)

Acorn’s top-tier plan is dubbed Acorns Premium and is geared towards families with children. Acorns Premium comes with everything that is included in Acorns Personal and Personal Plus, with the addition of:

| Acorns Premium Features (in Acorns’ own words) | My Impression |

| Investment account for kids | This is not a 529 account, but rather a UTMA/UGMA custodial account (Uniform Transfer to Minors/Uniform Gift to Minors). This means the money can be used for more than just education expenses, which is nice. However, these account types are free to open elsewhere. |

|

Customize your portfolio with the ability to add individual stocks

|

The fact that this is considered a premium feature is somewhat off-putting to me. This ability comes standard with almost any investing account anywhere. |

|

Get your bonus investments matched by Acorns (up to 50%)

|

Just a higher incentive for users to complete offers from Acorns’ partners. It might not be worth the extra $4 per month if this is all you are looking for. |

|

Educational courses

|

This is great, but it could lead to customers realizing that there are better options out there for them than Acorns. |

|

Banking for kids with GoHenry by Acorns, including a debit card, parental control, and chore tracker.

|

I don’t have kids yet, but this actually seems like a cool feature and a great way to teach your kids about money. This could potentially make the $9 a month worth it for me. |

|

$10,000 life insurance policy for eligible customers plus a no-cost will.

|

These are good things to have in place and are often overlooked, so I like that Acorns is trying to holistically service its clients beyond just investing. |

The Acorns Portfolios

Acorns isn’t really built for people who want to trade individual stocks or do anything sophisticated with their investments, which is something to be aware of if you are considering opening an account. Instead, Acorns has five “model portfolios” that are each built with a particular risk profile in mind.

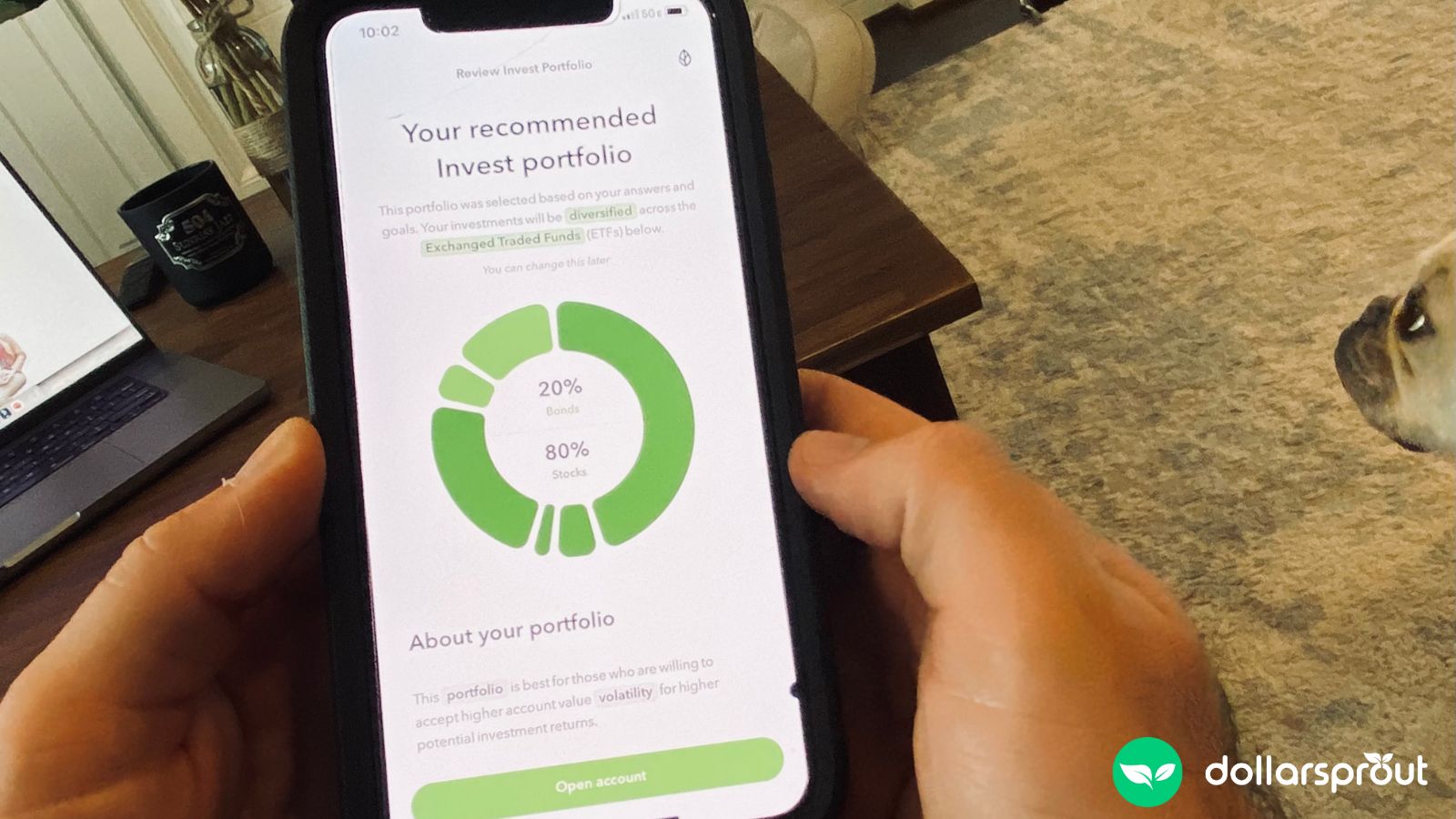

For instance, after I answered some basic questions about myself — things like my age, income, risk tolerance, etc. — and Acorns recommended a portfolio that consisted of 80% stocks and 20% bonds, which is moderately aggressive. This made sense based on my answers, so no complaints there. It is important to note, however, that if you have any special circumstances that fall outside the scope of their basic questions, there are no human advisors that you can speak to directly.

Acorns offers five different portfolios based on five levels of risk, and each one is composed of exchange-traded funds, or ETFs. Think of an ETF as a basket of many different stocks and bonds. In addition to the five core portfolios, Acorns also offers four ESG portfolios, which stand for “environment, social, and governance” issues. If these are causes you care about, you can elect to invest in an ESG portfolio instead; however, the expense ratios of the funds within these portfolios may be slightly higher.

Benefits

For people who are just starting out with investing and getting their financial lives in order, Acorns can be a decent choice. For those types of people, Acorns offers the following clear benefits:

- An all-in-one solution: Some people might get overwhelmed by having their money in so many different places. Acorns gives customers the opportunity to have pretty much everything within one central location, which can give some peace of mind.

- Tools for building strong financial habits: If the thought of regularly scheduled contributions to your investments feels constricting, the Round-Up feature is a neat way to achieve a similar outcome in a more psychologically appealing way. For some reason, it’s easier to digest the thought of investing $1 a day than it is to invest $30 at the end of each month.

- Cookie-cutter options, by design: Acorns wants you to be as hands-off as possible, unlike competitors like Robinhood, M1 Finance, etc. By recommending simple yet professionally constructed ETF portfolios, customers are less likely to risk financial ruin by diving into options trading and other speculative (and risky) trading strategies.

- Teaching your kids about money: For $9 a month, the Premium Plus plan is a good option for parents who want to invest in their children’s future, both financially and educationally. The debit card for kids and the chore tracker are great ways to prepare children for financial responsibility one day.

Drawbacks

No investment app or website can be everything to everyone, and Acorns is no exception. From my own investigation, these are a few of the biggest drawbacks of Acorns:

- The monthly fees are way too high, unless you are investing a large amount. As a general rule of thumb, you should aim for your yearly investing expenses to be less than 1% of your total portfolio value (at the most), but ideally, you should strive to get your investing expenses under 0.50%. With Acorns’ flat monthly pricing model, here’s what the math looks like:

- Personal ($36 per year): You would need a $7,200 portfolio for the yearly fees to be at 0.50% (not including the ~0.06% fees for the ETFs themselves).

- Personal Plus ($60 per year): You would need a $12,000 portfolio for the yearly fees to equal 0.50% (not including the ~0.06% fees for the ETFs themselves).

- Premium ($81 per year): You would need $18,000 invested in order for the yearly fees to equal 0.50% (not including the ~0.06% fees for the ETFs themselves).

- The bonus investments from the Acorns brand partners could be a conflict of interest. Acorns is financially incentivized to promote those offers to customers, which is something to be aware of when using the app.

- Lack of investment options. While some will see this as a good thing, I still can’t get over the fact that you have to be on the $9 a month Premium plan if you want to buy an individual stock for your portfolio.

- Transfers are expensive. Most brokerages charge a flat fee per account if a customer wants to transfer to another brokerage, but Acorns charges $50 per ETF. So, what is somewhere between free and $75 at most brokerages, Acorns charges $300 for the 6 ETF portfolio that it recommended for me. This essentially traps a lot of customers with Acorns. Not cool.

Who Is Acorns Best Suited For?

While the fees are prohibitively expensive, for some people, they may be worth it. Here is who I think would most benefit from Acorns:

- People who need to be forced into saving money. If the alternative is not saving money at all, I would rather someone pay the fees to Acorns to have everything taken care of for them.

- Parents who want to take an active role in teaching their kids about money. If you simply want to save for your children’s future, you can probably find better options. But if you want to give your child a debit card, teach them about budgeting, etc., I think the features offered with Acorns Premium are worth it.

- Investors with at least $10,000 to invest who desire a hands-off approach. If you are a passive investor and have at least five figures to put to work, the monthly fees charged by Acorns are in line with what other robo-advisors charge.

Acorns Alternatives

Acorn’s relatively high fees are reason enough for some investors to look elsewhere. If you have $10,000 or less to invest, these options may be more suitable for you.

Robinhood

Robinhood may be more appealing to investors interested in active trading and a wide variety of investment options, including stocks, cryptocurrencies, and options. Unlike Acorns, which focuses on passive, automated investing through round-ups and recurring investments, Robinhood provides a platform that encourages direct, commission-free trades, allowing investors more agility and flexibility in their transactions.

Key Differences:

- Investment Options: Robinhood offers extensive trading options, including stocks, options, and cryptocurrencies.

- User Interface: Robinhood has a user-friendly interface catered to investors who prefer a more active trading experience.

- Fees: Robinhood offers commission-free trades, while Acorns charges a monthly fee for its services.

- Taxes: No automated tax savings options (same as Acorns).

M1 Finance

M1 Finance might be more suitable for investors who seek customization and control over their investment portfolios, allowing them to select and allocate specific stocks and ETFs in a “pie” format. Additionally, it offers features like automatic rebalancing and fractional shares, making it appealing to both beginner and experienced investors who want a personalized yet automated investment experience.

Key Differences:

- Investment Options: M1 offers a wider range of investment choices, including individual stocks and ETFs.

- Rebalancing: Automatic rebalancing is a feature in M1 Finance to maintain the desired asset allocation.

- Fees: M1 Finance lacks the $3 to $9 monthly fee that Acorns charges, making it more cost-effective for some investors.

- Minimum Investment: M1 Finance has a higher minimum investment requirement ($100) compared to Acorns.

- Taxes: Tax Minimization Feature (similar to but not the same as traditional tax-loss harvesting).

|

$0 per trade |

$3 to $9 per month |

$0 per trade |

| Designed for DIY investors | Beginner-friendly | Commission-free trading |

| Easy-to-use mobile app | Completely automated | Automated rebalancing |

| No account minimum | No account minimum | $100 account minimum |

|

Get 1 free stock |

$20 sign-up bonus |

No sign-up bonus |

Verdict: Is Acorns Worth It?

When it comes to round-up investing apps, Acorns is among the best in the business, but it might not be right for everyone. It’s easy to use, has an excellent education platform for new investors, and simple, straightforward fees.

However, whether the $3 to $9 monthly fee is a benefit or a detriment really depends on your account balance. If you’re only adding a few dollars a month to your Acorns account, the $3 a month fee will hinder your investment growth.

Related: