How to Start Investing: The Ultimate Beginner’s Guide (2024)

Our readers always come first

The content on DollarSprout includes links to our advertising partners. When you read our content and click on one of our partners’ links, and then decide to complete an offer — whether it’s downloading an app, opening an account, or some other action — we may earn a commission from that advertiser, at no extra cost to you.

Our ultimate goal is to educate and inform, not lure you into signing up for certain offers. Compensation from our partners may impact what products we cover and where they appear on the site, but does not have any impact on the objectivity of our reviews or advice.

Stashing money away in a savings account isn't enough to build wealth. A bank may keep your money safe, but each year, inflation makes every dollar worth less. You can beat inflation and build wealth over time by investing some of that money. Here's how.

Our mission at DollarSprout is to help readers improve their financial lives, and we regularly partner with companies that share that same vision. If a purchase or signup is made through one of our Partners’ links, we may receive compensation for the referral. Learn more here.

Do you want your money to earn you more money?

Well, it can’t do its work hiding in a bank account. Whether you want to save for your child’s college or prepare for retirement, you’ll reach your goal faster by investing.

Here’s everything you need to know about how to start investing, today.

What Is Investing?

When you invest, you purchase something with the expectation of profiting off of it in the future.

In the 1990s, some people thought they were making smart “investments” in Beanie Babies and McDonald’s toys. But traditional investments include things like ownership in a business, real estate assets, or lending money to a person or company in exchange for interest payments.

Why Should I Invest?

Merely saving money isn’t enough to build wealth. A bank will keep your money safe. But, each year, inflation makes every dollar you’ve tucked away slightly less valuable. So, a dollar you put in the bank today is worth just a little less tomorrow.

Comparatively, when you invest, your dollars are working to earn you more dollars. And those new dollars work to earn you even more dollars. The snowballing force of growth is known as compound growth.

Over the long term, investing allows your assets to grow over and above the rate of inflation. Your past savings build on themselves, instead of declining in value as the years pass. This makes it significantly easier to save for long-term goals like retirement.

Related: 15 Expert Tips for Beating Inflation

When Should I Start Investing?

Yesterday. But if you haven’t started yet, today is a great second choice.

In general, you want to start investing as soon as you have a solid financial base in place. This includes having no high-interest debt, an emergency fund in place, and a goal for your investments in mind. Doing so allows you to leave your money invested for the long-term – key for maximum growth – and be confident in your investment choices through the natural ups and downs of the market.

Benefits of starting young

Compound growth requires time. The earlier you start investing, the more wealth you can create with fewer dollars.

When it comes to investing, time is your most powerful tool. The longer your money is invested, the longer it has to work to create more money and take advantage of compound growth. It also makes it far less likely that one harsh market downturn will negatively impact your wealth as you’ll have time to leave the money invested and recover its value.

Let’s look at an example:

Since 1928, the average return of the S&P 500 (a set of 500 of the largest public companies in the U.S. that is often used to approximate the stock market) is about 10%.

So, let’s say you’re 25 and put $5,000 in the S&P 500. You see a 10% increase in value each year, letting your money continue to grow. When you turn 65, you open your account to find you have over $226,000. An excellent retirement gift to yourself!

However, if you waited until you were 35 to start investing, your value at 65 would only be $87,000. Still impressive, but fewer than half of what you would have had if you started a decade earlier.

Pay off high-interest debt first

View paying down high-interest debt as investing until you no longer have those debts. Every dollar toward principal earns you an instant return by eliminating future interest cost.

If you still have high-interest debt, such as credit cards or personal loans, you should hold off on investing. Your money works harder for you by eliminating that pesky interest expense than it does in the market. This is because paying off $1 of debt balance saves you 12%, 14%, or more in future interest expense. More than traditional investments can be expected to return.

Focus on getting out of debt as fast as you can, then dive into investing.

Have an emergency fund in place

To reduce the risk of having to pull money out of your investments early, have an emergency fund to protect from life’s unexpected twists and turns.

Remember how we said time is the most powerful tool? To start investing, you have to be set up to let that money stay invested. Otherwise, you limit your time horizon and could force yourself to withdraw your money at the wrong time.

To protect yourself from unexpected expenses or job layoffs, save a sufficient emergency fund for your needs. Do not plan for your investment accounts to be a regular source of cash.

Starting small is OK

Sometimes people think they can’t start investing until they have a significant amount of money. But this means many people give up years of compound growth waiting until they feel rich enough. No matter how small, get your money working for you as soon as possible.

Consider our previous example of the $5,000 invested at 25- or 35-years-old. Pretend for a moment the 35-year-old didn’t have $5,000 to invest at age 25, but she did have $500. And she thought, maybe, she could scrape together $50 a month to add to her $500 investment.

If she invested $500 at age 25, and then $50 a month until she had put away a total of $5,000, she would have almost $174,000 at retirement age. That is double what she would have had if she waited until she had $5,000 at age 35.

Starting small makes a significant difference, especially if it means you get in the market sooner.

Investing 101: Basic Investing Terms

The number one thing that scares off new investors is the jargon. The investment market has a ton of jargon. So, we’re going to give you the inside scoop to make it less intimidating.

What is a stock?

A stock, also known as a “share,” is a tiny ownership stake in a business. Public companies allow anyone to buy or sell ownership shares of their business on exchanges.

If you own a stock, you are actually a part owner of the company. Go you! While owning a share of Walmart won’t give you the power to fire the slow cashier at your local store, you do have some rights. You can, for instance, vote on members of the Board of Directors.

What is a bond?

A bond is debt of a corporation, municipality, or country.

By purchasing a bond, you are loaning money to one of these entities. For companies, bonds are typically segmented into $1,000 increments that pay interest every six months, with the full value paid back at “maturity,” i.e., the date the debt is due. Government bonds are typically known as “treasuries.”

What is a portfolio?

A portfolio is a collection of all your investments held by a particular broker or investment provider. You may own some individual stocks, bonds, or ETFs. Everything in your account would be your portfolio.

However, your portfolio can also mean all your investments across all account types, as this gives a better picture of your entire exposure.

What does diversification mean?

Just like you wouldn’t invest all your money in your friend’s idea for a pumpkin-spiced toothpaste business, you don’t want to only invest in one stock or bond. Diversification means owning a variety of different investments, so your success or failure isn’t dependent on just one thing.

To be properly diversified, you want to make sure your investments actually have variety. Owning three different clothing companies still means you’re facing all the same risks. An import tax on cotton products, for example, could crush the value of all three companies at once.

What is asset allocation?

There are three main asset classes for most investors: stocks, bonds, and cash. Asset allocation is how you split your investments across those three buckets.

Stocks offer greater long-term returns, but significantly greater swings in value. These swings, sometimes north of 20% up or down in a given year, can be a lot to stomach. Bonds are safer but provide lower returns in exchange for that security.

You determine your asset allocation by considering the length of time until you need your money, your risk tolerance, and goals.

What are ETFs?

ETFs, or exchange-traded funds, allow you to buy small pieces of many investments in one security.

An ETF is a fund that holds numerous stocks, bonds, or commodities. The fund is then divided into shares which are sold to investors in the public market.

ETFs are an attractive investment option because they offer low fees, instant diversification, and have the liquidity of a stock (they are easy to buy and sell fast). Buying a stock or bond ETF gives you access to numerous investments, all held within that ETF.

Stock funds

A stock ETF often tracks an index, such as the S&P 500. When you buy a stock ETF, you are purchasing a full portfolio of tiny pieces of all the stocks in the index, weighted for their size in that index.

For instance, if you purchased an S&P 500 ETF, you are only buying one “thing”. However, that ETF owns stock of all 500 companies in the S&P, meaning you effectively own small pieces of all 500 companies. Your investment would grow, or decline, with the S&P, and you would earn dividends based on your share of the dividend payouts from all 500 companies.

Bond funds

A bond ETF owns a basket of bonds, often tracking an index, just like the stock ETFs.

These funds could own a mixture of government bonds, high-rated corporate bonds, and foreign bonds. The most significant difference between holding an individual bond and a bond ETF is when you are paid interest. Bonds only make interest payments every six months. Bond ETFs make payments every month, as all the bonds the fund owns may pay interest at different times of the year.

Types of Investment Accounts

If you’re ready to buy stocks, bonds, or ETFs, you may be wondering where these types of investments are held.

There are a few different types of accounts in which you can hold investments. But they can’t live in your standard bank account. Here are your options.

Retirement accounts

Saving for retirement is most people’s biggest long-term goal. With the average person retiring at 62, either by choice or due to layoffs and health issues, most Americans face 20 years or more of retirement in which they need assets to support themselves.

To help you prepare for this massive goal, the government offers tax incentives. However, if you invest in these accounts, your access to your funds is limited until 59 ½. In some cases, there are penalties for withdrawing your money earlier.

Here are the type of accounts that offer tax savings.

Employer-sponsored accounts

Employer-sponsored retirement accounts such as 401(K)s, 403(B)s, 457s, and more, allow employees to save for retirement directly from their paycheck. Some employers offer contribution matches as a perk to double-down on your retirement preparation.

Typically, you put “pre-tax” money into these accounts, which means you don’t pay income tax on those dollars. Any money invested grows without tax until you ultimately withdraw it for living expenses in retirement. As you withdraw funds, you will pay income tax on the withdrawals. However, most people are in a lower tax bracket in retirement so pay lower rates.

As of 2020, you can contribute up to $19,500 in a given year to one of these accounts, not including any employer contribution. If you are 50 years or older, you can contribute up to $26,000 a year.

Traditional vs. Roth IRA

If you don’t have access to an employer-sponsored retirement account or have already maxed out your contribution, you can also open an Individual Retirement Account (IRA) to invest.

There are two types of IRAs: Traditional and Roth.

A Traditional IRA works the same way as employer-sponsored plans when it comes to taxes. Any money contributed will be treated as “pre-tax” and reduce your taxable income for that year.

A Roth IRA, on the other hand, is funded with post-tax dollars. This means you’ve already paid your income tax, so when you withdraw it in retirement, you don’t pay income or capital gains tax. The money is all yours. Roth IRAs offer excellent tax benefits but are only available to certain income levels. If you make more than $135,000 a year as a single filer or over $199,000 as a married filer, you aren’t eligible for a Roth IRA.

As of 2020, you can contribute up to $6,000 per year to an IRA. If you are 50 years or older, you can contribute up to $7,000 a year.

529 college savings plans

These accounts, offered by each state, provide tax benefits for parents saving for college. Operating like a Roth IRA, contributions are made post-tax, but all withdrawals are tax-free as long as the funds are used for higher-education expenses.

Your state may offer tax benefits or contribution matches for investing in your local 529 plan, but you can utilize any state’s 529. Since each state has different fees and investment options, be sure to find the best 529 for your money.

Brokerage accounts

Brokerage accounts offer no tax benefits for investing but operate more like a standard bank account to hold your investments. There are no limits on annual contributions to these accounts, and you can access your money at any time.

|

$0 per trade |

$1-3 per month |

$0 per trade |

| Designed for DIY investors | Beginner-friendly | Commission-free trading |

| Easy-to-use mobile app | Completely automated | Automated rebalancing |

| No account minimum | No account minimum | $100 account minimum |

|

Get 1 free stock |

$10 signup bonus |

No signup bonus |

Cash or cash equivalents

Since investing should only be undertaken for the long-term, you may need to hold onto cash while saving for shorter-term goals. In that case, a traditional bank account might not do the trick. Checking and savings accounts offer incredibly low interest rates, if any at all, which means you are entirely at the mercy of inflation.

Luckily, there are cash accounts that pay higher interest:

A CD, or Certificate of Deposit, is a savings account that restricts access to your cash for a specified period (6 months, 12 months, 24 months, etc.). There is a small penalty if you want to withdraw your money before the term is up, but these accounts typically offer a higher interest rate in exchange for the lack of access.

High-yield online savings accounts are the middle ground between CDs and traditional savings accounts. They pay higher interest than a conventional savings account but still allow a few transactions a month so you can access your cash if you need it. Many online high yield savings accounts have no deposit minimums or fees.

Money market accounts are very similar to high yield savings accounts, but with slightly higher interest rates and higher deposit requirements. For instance, CIT Bank’s money market account offers a 1.85% interest rate but requires a $100 minimum deposit.

In any of these accounts, your cash deposited is not at risk. FDIC insurance guarantees you your money back, even if the bank that holds your account goes bankrupt.

Related: Best Online Savings Accounts for 2024

Where to Focus First

When first starting to invest, it can be hard to choose between the multiple types of investment accounts. As you begin, remember to focus where you see the most value.

First, contribute enough to your employer-sponsored retirement plan to get the full value of any match the company offers. This is free money and an instant return on your investment. If you aren’t sure if your employer offers a contribution match, reach out to HR for the most up-to-date policies.

Second, max out contribution limits on your tax-advantaged accounts – if you are primarily saving for early retirement or a child’s college. The tax benefits in these accounts save you money that you don’t want to turn over to Uncle Sam unnecessarily.

Finally, invest any excess capital in brokerage accounts. This will help you save for long-term goals like buying that vacation house in ten years.

Note: The above assumes that you have paid off all high-interest debt and have a solid budget in place. If you haven’t done those things yet, get them squared away before you start investing.

7 Golden Rules for Investing Money

You may be a rookie investor, but that doesn’t mean you need to make costly rookie mistakes. Follow these seven golden rules and you’ll be on the path to success.

Click here to see the whole infographic.

1. Play the long game

Never invest for the short-term. The market moves up and down in natural cycles that can’t be timed. Investing for fewer than three to five years doesn’t give you enough time to rebuild asset value if you hit a downturn at the wrong time.

2. Don’t put all your eggs in one basket

Don’t put too much of your money in any one stock or bond where one issue could destroy your wealth. Diversify with low-cost, index ETFs and avoid stock picking.

3. Make investing a monthly habit

Despite headlines continually calling a market top or bottom, no one can accurately determine where we are in the cycle at any given time. The best way to guarantee that you buy at the right times is to make investing a monthly habit. Invest each and every month, regardless of headlines or market performance.

Related: How to Get Started Investing with $100

4. Invest only what you can afford to lose

Investing is risky. While the long-term trend has historically been upwards, there are also years of deep declines. If you need money in the near-term, or the thought of seeing your account balance drop 20% makes you sick to your stomach, don’t invest those funds.

5. Don’t check your portfolio every day

Investing is the one place where a “head in the sand” strategy might be the smartest method. Set up auto deposits into your investment accounts each month and only look at your portfolio once every three to six months. This reduces the likelihood of panic selling when the market falls or piling in more money when everything seems like rainbows and butterflies.

6. Keep your fees low

Mutual funds and ETFs have expense ratios. Many brokerages charge trading fees. Investment providers from financial advisors to robo-advisors charge management fees. All these fees eat away at your wealth over time.

Sticking to index funds and ETFs keeps your fees low while guaranteeing you see the performance of the market so that you can keep more money in your pocket.

7. Listen to Warren Buffet’s investing advice

Warren Buffett is possibly the most famous investor in history. He’s created a multi-billion-dollar net worth in just one generation. Learn from his advice to invest for your own future.

“Someone is sitting in the shade today because someone planted a tree a long time ago.”

“I never invest in anything I don’t understand.”

“If you don’t find a way to make money while you sleep, you will work until you die.”

“The stock market is a device for transferring money from the impatient to the patient.”

“It is not necessary to do extraordinary things to get extraordinary results.”

How to Start Investing Today

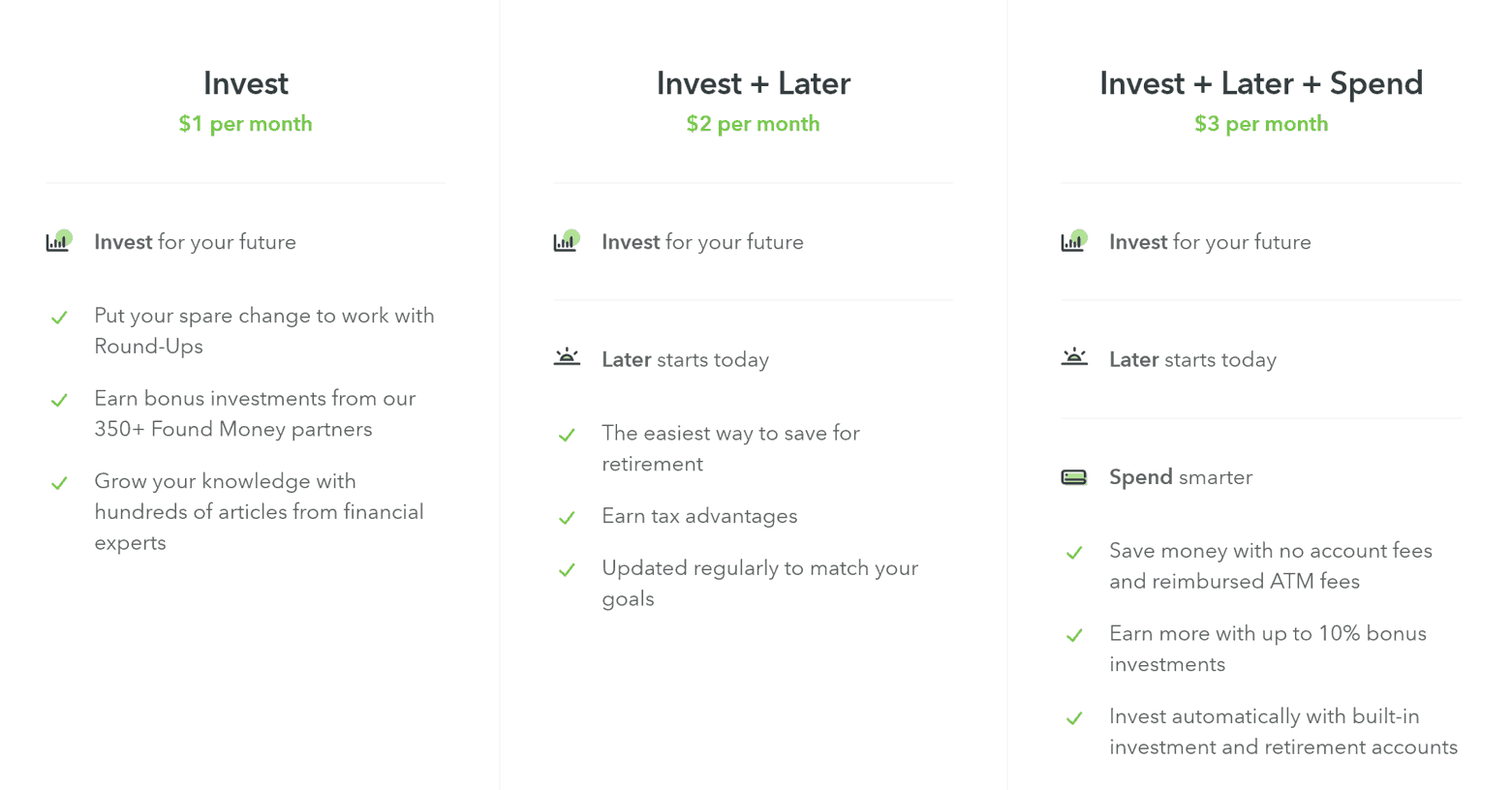

An easy way to start investing today from your phone or laptop is by opening an account with Acorns, a micro-investing app ideal for beginner investors.

The basic plan, Acorns Invest, starts at just $1/month with a free $10 sign-up bonus for new users.

When you make a purchase with a linked debit or credit card, Acorns rounds up to the nearest dollar and invests your spare change. You can boost your Round-Ups by 2x, 5x, or 10x.

In addition to Round-Ups, you can set up recurring daily, weekly, or monthly investments to your Acorns portfolio. Its Found Money service will also find cashback opportunities from 200+ partners and automatically invest your savings when you make a purchase.

It only takes a few minutes to set up an account. Once you complete your profile, Acorns suggests one of its five portfolio options based on the information you provided. However, you have the option to override its suggestion if you prefer a portfolio with more or less risk.

The platform automatically rebalances your portfolio and reinvests all dividend payments to continue growing your investments.

Acorns is a smart option for hands-off investors and those just getting started. As your account grows, the $1-3 monthly fee stays the same, effectively making the service cheaper over time.